Institutional Insights: JPMorgan Nvidia, Investment Thesis, Valuation & Risks

.jpeg)

Investment Thesis, Valuation and Risks

NVIDIA Corporation

(Overweight; Target Price: $170.00)

Investment Thesis

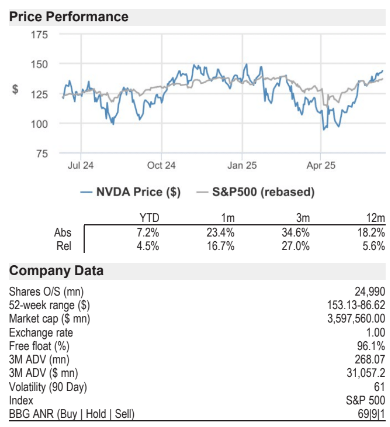

We believe NVIDIA is effectively executing across all its segments. Although the first half of the year is usually weaker than the second half, we anticipate robust demand in the PC gaming sector to significantly boost the company's revenue, compensating for the decline in PC OEM, which is experiencing a long-term downturn. We expect strong growth in the data center division as hyperscale clients increasingly adopt GPU-accelerated deep learning for processing vast data sets. We are also optimistic about the robust performance in the automotive and enterprise sectors, although widespread adoption of autonomous driving in the market is still uncertain. We foresee considerable upside potential for the shares, justifying our Overweight rating.

Valuation

Our December 2025 price target of $170 is based on the assumption that NVIDIA trades at a multiple of 30 times our projected earnings of $5.39 for the calendar year 2026. This earnings multiple aligns with a potential earnings compound annual growth rate (CAGR) of over 30-35% in the coming years, driven by continued strong growth in the data center segment, tapping into an additional ~$14 billion in automotive revenue, and increasing revenues from software, licensing, and subscriptions over the next several years.

Risks to Rating and Price Target

- While demand for PC gaming appears resilient against macroeconomic challenges, any economic uncertainty could negatively affect PC gaming trends. With NVIDIA’s ~53% exposure to this segment, weakness in consumer PC gaming presents a downside risk to our projections.

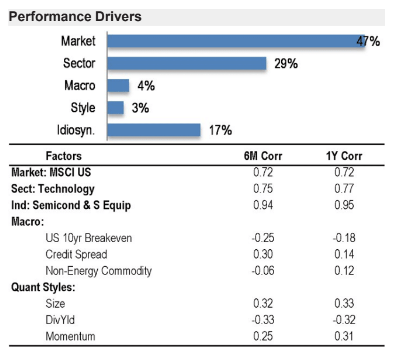

- NVIDIA’s GPUs may see lower-than-expected adoption in data center applications as hyperscale clients increasingly embrace deep learning for processing extensive unstructured data. A significant decline in deep learning adoption by these customers or a surge in competition could pose a downside risk to our revenue and earnings forecasts.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!